I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.

See all posts Frank GogolAnalysis: Mississippi Borrowers Impacted Worst by Student Debt

Updated on April 8, 2024

Written by

Written by

In a recent comprehensive analysis of student loan data, some startling revelations about the state of educational debt in the United States have come to light. Through meticulous examination of borrower data, paired with state population and economic figures, a clearer picture of the student debt landscape has emerged.

Key Findings

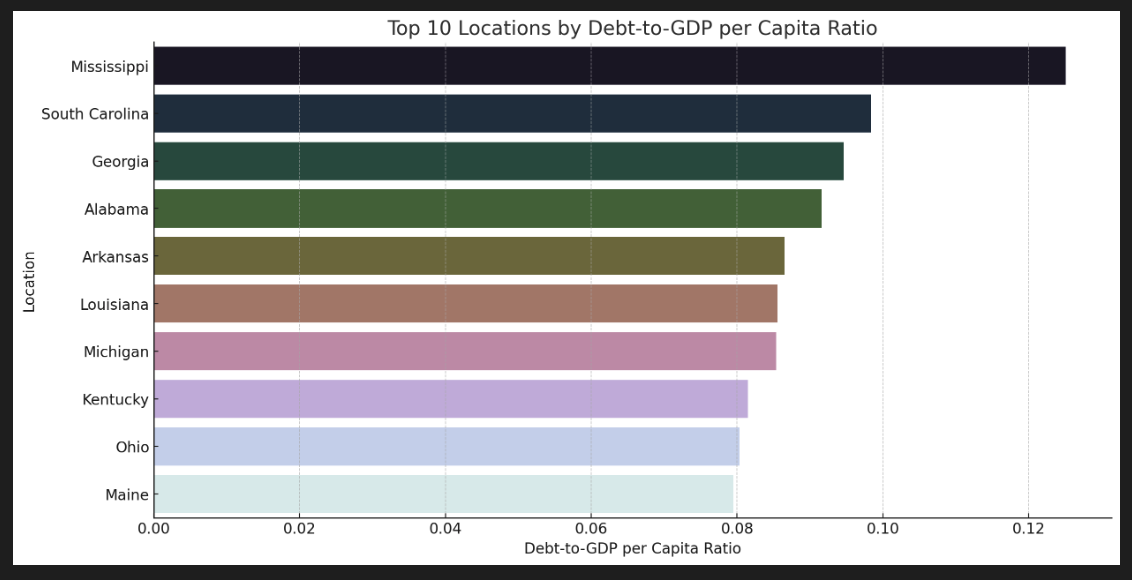

- Mississippi has the highest per capita student loan debt relative to economic output (Debt-to-GDP per capita ratio) at 12.51%.

- The state’s Debt-to-GDP per capita ratio is 2.67% higher than South Carolina’s, the next highest state.

- Mississippi’s Debt-to-GDP per capita ratio exceeds the national average by 5.67%.

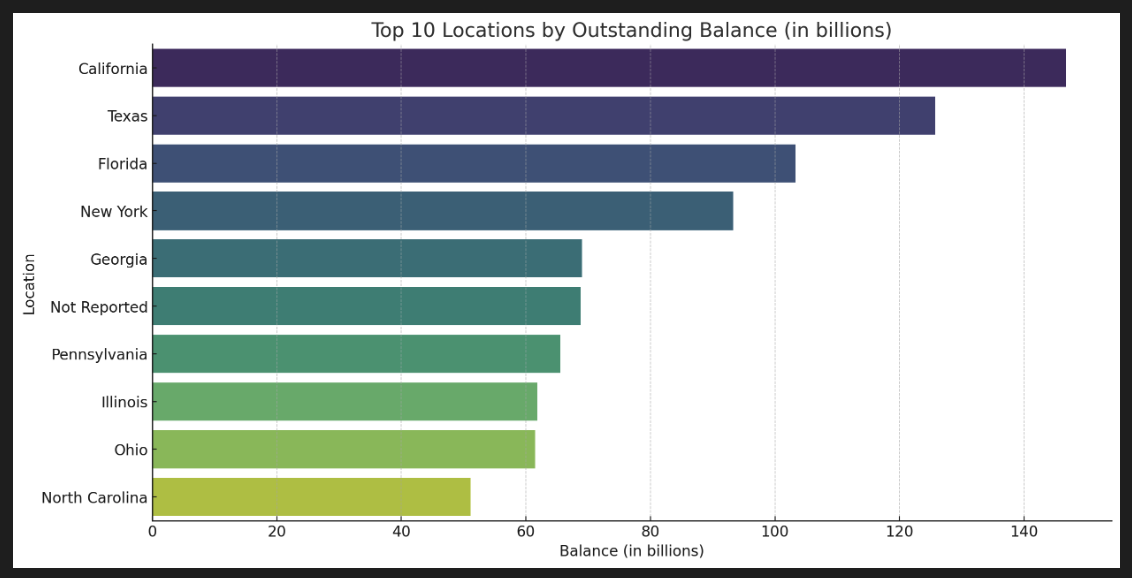

A Geographic Breakdown

Initially, our analysis focused on the geographical distribution of

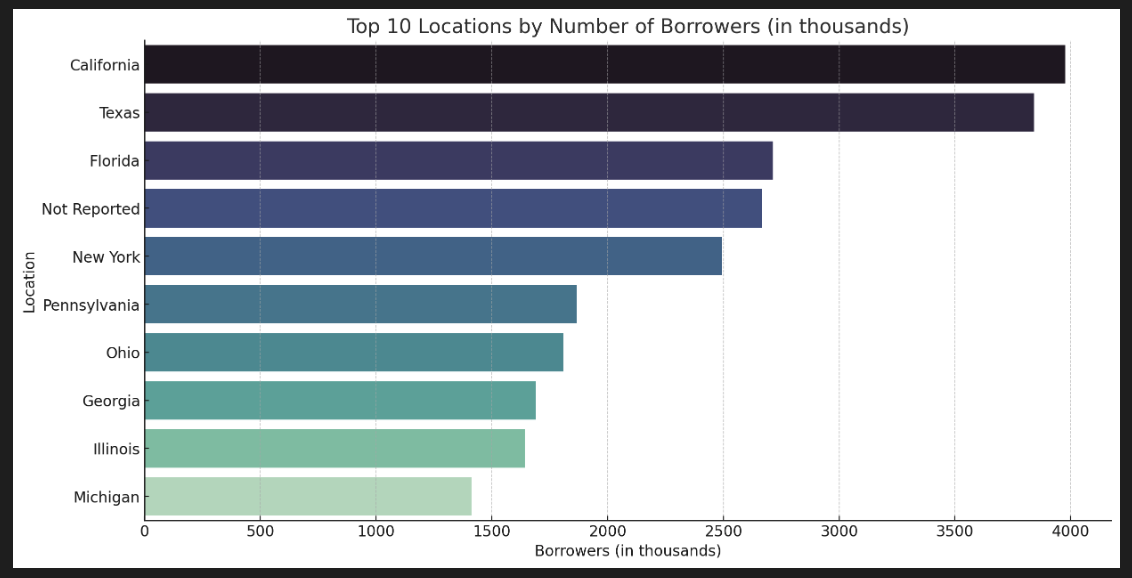

California’s outstanding student loan balance is staggering 16.71% greater than the next highest state, Texas, but with just 3.5% more borrowers. But given the vast population and economic disparities across different states, these numbers are just part of the story.

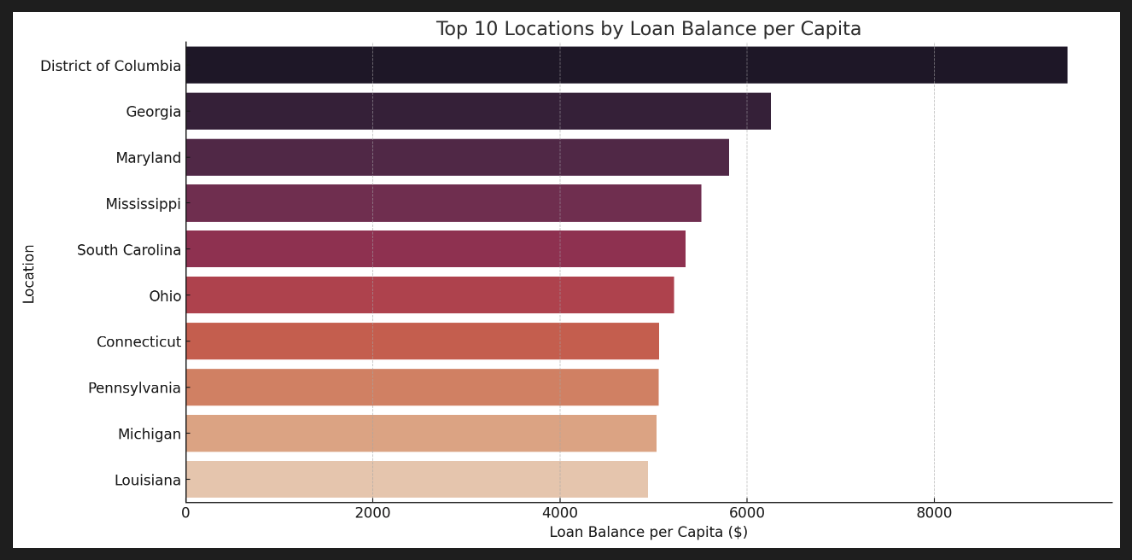

Loan Balance Per Capita and Borrower Ratio

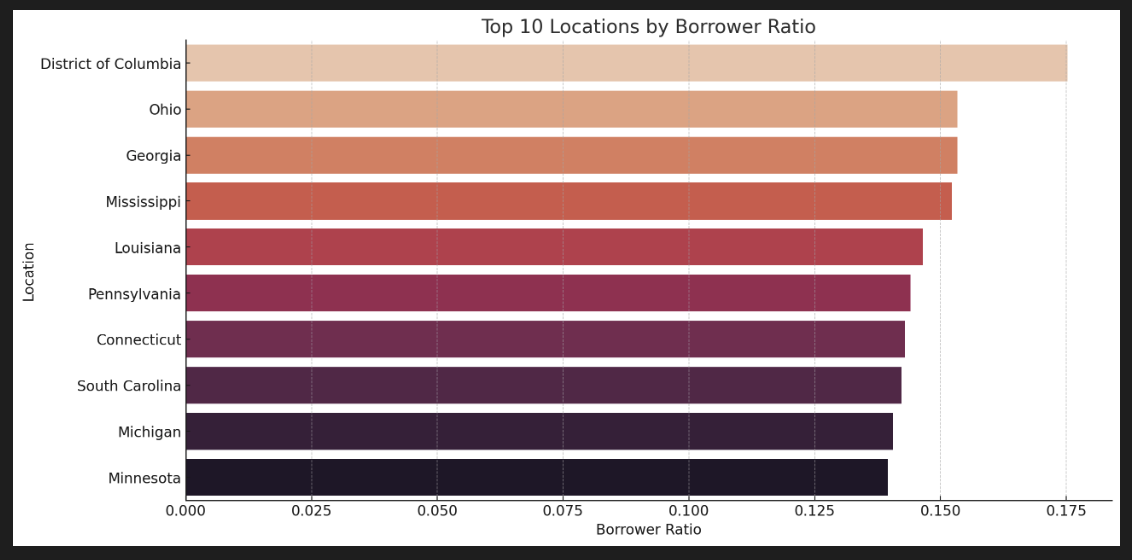

To account for varying state populations, loan balance per capita and borrower ratios were calculated using state population estimates from the U.S. Census Bureau (via StatsAmerica.org). The District of Columbia startled everyone with its figures, showing the highest debt load per person as well as the highest percentage of its population having student

This suggests that, relative to its size, D.C. faces a disproportionately high student debt burden. But since D.C. is in the bottom three of population size (678,972) and the bottom seven of GDP per capita ($233,500), further analysis was required to find out the economic impact of debt-to-GDP per capita on borrowers across the U.S.

Economic Pressure Points

When state Gross Domestic Product (GDP) per capita data for 2023 was introduced, a new metric emerged: the Debt-to-GDP per capita ratio. This ratio reflects the size of student debt relative to individual economic output, offering insight into the potential pressure of debt on economic well-being.

Mississippi, often overshadowed in economic discussions, stood out with the highest Debt-to-GDP per capita ratio.

The bar chart shows the top 10 locations by Debt-to-GDP per capita ratio. A startling 12.51% of the state’s GDP per capita is equivalent to student debt per person, showing that student

Below, we’ve compiled all of the data into a single table, ranking states from highest Debt-to-GDP per capita ratio to lowest:

| Location | Loan Balance per Capita | GDP Per Capita | Debt-to-GDP per Capita |

| Mississippi | $5,510.79 | $44,060 | 12.51% |

| South Carolina | $5,340.97 | $54,280 | 9.84% |

| Georgia | $6,256.10 | $66,109 | 9.46% |

| Alabama | $4,678.51 | $51,086 | 9.16% |

| Arkansas | $4,302.85 | $49,732 | 8.65% |

| Louisiana | $4,941.24 | $57,769 | 8.55% |

| Michigan | $5,031.25 | $58,935 | 8.54% |

| Kentucky | $4,418.76 | $54,216 | 8.15% |

| Ohio | $5,218.08 | $64,941 | 8.04% |

| Oregon | $5,242.11 | $65,806 | 7.96% |

| Maine | $4,585.44 | $57,699 | 7.95% |

| Maryland | $5,808.82 | $73,313 | 7.92% |

| West Virginia | $4,067.63 | $51,573 | 7.89% |

| Missouri | $4,696.46 | $60,489 | 7.76% |

| Florida | $4,568.63 | $59,046 | 7.74% |

| Vermont | $4,479.01 | $58,311 | 7.68% |

| Pennsylvania | $5,053.36 | $67,485 | 7.49% |

| New Mexico | $3,941.55 | $54,200 | 7.27% |

| Arizona | $4,265.72 | $59,071 | 7.22% |

| Rhode Island | $4,472.30 | $62,817 | 7.12% |

| Idaho | $3,664.63 | $51,793 | 7.08% |

| Virginia | $4,933.63 | $71,133 | 6.94% |

| New Hampshire | $5,074.98 | $73,751 | 6.88% |

| Montana | $3,795.86 | $56,130 | 6.76% |

| Oklahoma | $3,703.81 | $54,824 | 6.75% |

| Indiana | $4,298.91 | $64,357 | 6.68% |

| New Jersey | $4,956.86 | $75,549 | 6.56% |

| North Carolina | $4,204.24 | $64,885 | 6.48% |

| Colorado | $4,899.95 | $75,860 | 6.46% |

| Illinois | $4,924.42 | $76,825 | 6.41% |

| Tennessee | $3,985.33 | $62,944 | 6.33% |

| Kansas | $4,250.91 | $67,570 | 6.29% |

| Minnesota | $4,653.26 | $75,234 | 6.19% |

| Wisconsin | $3,941.83 | $64,436 | 6.12% |

| Connecticut | $5,059.20 | $85,609 | 5.91% |

| Utah | $4,072.21 | $69,007 | 5.91% |

| Iowa | $4,084.81 | $70,683 | 5.78% |

| Delaware | $4,845.48 | $83,922 | 5.77% |

| Texas | $4,115.92 | $71,274 | 5.77% |

| South Dakota | $3,982.07 | $70,148 | 5.68% |

| Nevada | $3,550.20 | $64,983 | 5.47% |

| Nebraska | $3,993.17 | $78,500 | 5.09% |

| New York | $4,886.37 | $96,502 | 5.06% |

| North Dakota | $4,233.74 | $85,647 | 4.94% |

| Hawaii | $3,205.27 | $65,857 | 4.87% |

| Massachusetts | $4,541.95 | $95,029 | 4.78% |

| California | $3,764.90 | $89,540 | 4.20% |

| Alaska | $3,272.40 | $79,139 | 4.14% |

| District of Columbia | $9,426.01 | $233,500 | 4.04% |

| Washington | $3,635.02 | $90,034 | 4.04% |

| Wyoming | $2,910.67 | $76,577 | 3.80% |

The Disparate Impact

The Debt-to-GDP per capita ratio provides a perspective on the economic burden of student loan debt in relation to the overall economic output per resident in each state. A higher ratio indicates that the average student loan debt is a larger part of the economic activity of an average resident. This can be important for understanding the economic pressure that student loan debt might place on the residents of a state.

In Mississippi’s, where the Debt-to-GDP per capita ratio has hit a hefty 12.51%, this is especially true. This statistic isn’t just a number; it’s a clarion call highlighting the profound economic and societal implications of student debt within the state.

Economic Vulnerability

Mississippians grappling with student

Barriers to Personal Financial Milestones

The dream of homeownership, entrepreneurial ventures, or a comfortable retirement seems increasingly out of reach for those burdened by student debt. As young professionals in Mississippi dedicate a substantial slice of their income to servicing this debt, achieving these milestones becomes a delayed, if not elusive, goal.

The Workforce and Educational Impact

The ripple effects of high student debt extend into the workforce, influencing career paths and potentially leading to mismatches between job roles and individuals’ education or aspirations. This misalignment not only affects personal job satisfaction but also has broader implications for workforce development and economic productivity.

Social Mobility and Mental Health

The burden of student

Economic Growth at Risk

Beyond the individual level, high levels of student debt pose a threat to broader economic growth. As disposable income shrinks under the weight of loan payments, consumer spending—and by extension, economic activity—slows, hampering recovery and growth.

About This Data

The insights and analyses shared in this blog were derived from a detailed examination of student loan data alongside crucial state-level economic indicators such as population size and GDP per capita. By integrating these datasets, we were able to explore the multifaceted impact of student debt across the United States, revealing its economic implications.

Data Sources

The foundational data for this analysis were sourced from the following reputable entities:

- Federal Student Loan Portfolio – Portfolio by Location: This dataset, available at studentaid.gov, provided comprehensive information on the total loan balance and the number of borrowers, categorized by geographical location.

- U.S. Census Bureau – Population Estimate for 2023: State population figures were obtained from the U.S. Census Bureau, which offers a yearly estimate of population sizes. The specific data used can be found at statsamerica.org.

- GDP Growth Rate by State: Economic productivity, measured as GDP per capita by state, was sourced from wisevoter.com, providing a snapshot of economic output relative to the population.

Methodology

The analysis of student loan data alongside state-level population and GDP per capita figures employed a multi-faceted approach to uncover the intricate relationship between student debt and economic indicators across the United States. This section details the methodology behind the analyses conducted, providing a window into the process of extracting meaningful insights from the raw data.

Data Preparation and Cleaning

The first step in the analysis involved preparing and cleaning the datasets obtained from the Federal Student Loan Portfolio, U.S. Census Bureau, and GDP growth rate sources. This process included standardizing the format of location names, converting monetary and population figures into consistent units (e.g., converting loan balances to per capita terms), and ensuring accurate matching between datasets for each state.

Calculation of Key Metrics

- Loan Balance per Capita: This metric was derived by dividing the total outstanding loan balance by the state population, providing an average debt load per resident. It allowed for a comparison of the debt burden across states, normalized by population size.

- Borrower Ratio: The number of borrowers in each state was divided by the state population to calculate the proportion of residents with outstanding student

loans , highlighting the prevalence of student loan borrowers. - Debt-to-GDP per Capita Ratio: To assess the economic impact of student debt, the loan balance per capita was divided by the GDP per capita for each state. This ratio reflects the burden of student loan debt relative to the state’s economic output per person.

Frank Gogol

I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.