I’m a firm believer that information is the key to financial freedom. On the Stilt Blog, I write about the complex topics — like finance, immigration, and technology — to help immigrants make the most of their lives in the U.S. Our content and brand have been featured in Forbes, TechCrunch, VentureBeat, and more.

See all posts Frank GogolHow to Cancel a Venmo Payment

Updated on June 8, 2024

Written by

Written by

Reviewed by

Rohit Mittal

Reviewed by

Rohit Mittal

Rohit Mittal is the co-founder and CEO of Stilt. Rohit has extensive experience in credit risk analytics and data science. He spent years building credit risk and fraud models for top U.S. banks. In his current role, he defines the overall business strategy, leads debt and capital fundraising efforts, leads product development, and leads other customer-related aspects for the company. Stilt is backed by Y Combinator and has raised a total of $275M in debt and equity funding to date.

See all posts Rohit Mittal

At a Glance:

Venmo is a mobile payment service used for small transactions between individuals and businesses.

Unfortunately, Venmo payments cannot be canceled once made.

However, if you sent money to the wrong person or made a duplicate payment, you can request a refund or contact Venmo Support for assistance.

Venmo is a popular peer to peer payment app (one of the most popular in the US). It’s popular among the younger population that split payments with friends. Sometimes, we don’t realize and mistakenly transfer the payment to the wrong person and want to cancel the transaction.

Note:

Canceling a Venmo payment that you sent is different than declining or rejecting a payment sent to you. If you received an unwanted payment, you can send it back to the sender (after you receive it) but can’t decline or reject it.

How to Cancel a Venmo Payment

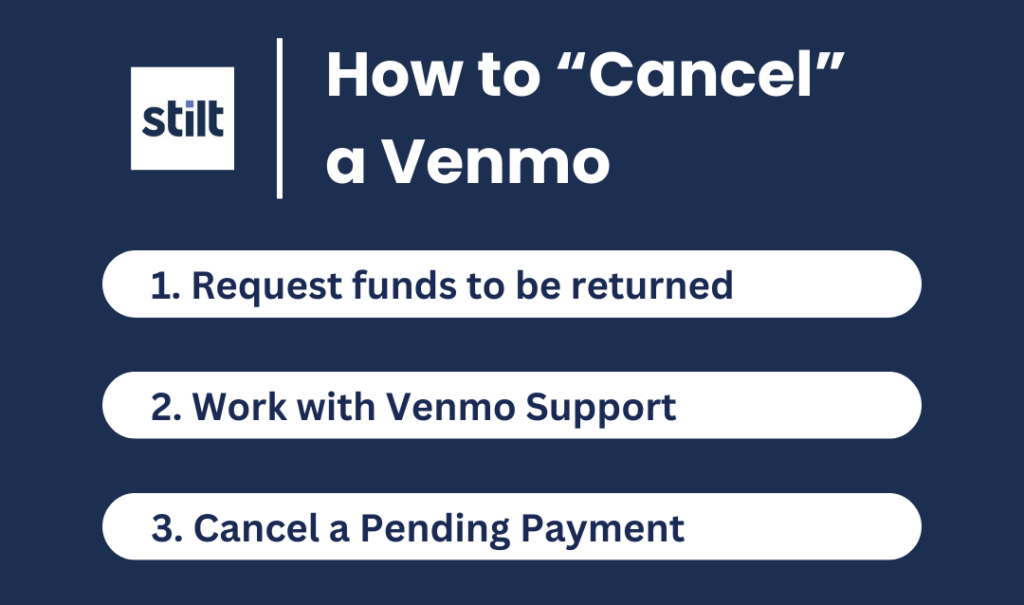

Unfortunately, once you’ve sent a payment to an existing account, it can’t be cancelled. The funds are immediately accessible to the recipient. That said, there are still ways to get your money back:

Issues with Sent Venmo Payments: When You Can Cancel

There are a few scenarios for needing to cancel Venmo payments that you have sent. Below, we’ll walk you through the most common situations:

1. Duplicate or Erroneous Payment

If you’ve sent money to someone you know more than once or mistakenly, simply ask the recipient to return the extra amount. After receiving the returned payment, you can move those funds from your account to your bank.

2. Reversal by Support

The Venmo team can only reverse a payment under specific circumstances:

- The recipient’s account maintains good standing.

- The funds are still present in their account.

- They give explicit permission to return the payment.

The Venmo team won’t reverse payments merely based on the sender’s appeal.

3. Wrong Recipient

If you suspect you’ve been scammed or mistakenly paid someone unfamiliar, reach out to the Venmo support team immediately. Please be aware that raising a dispute won’t automatically resolve this issue.

4. Pending Payment Status

Payments sent to an unregistered phone number or email will appear in the “Pending” section, where you have the option to cancel them. If you’ve made payments through iMessage, the process might differ.

Issues with Received Venmo Payments

There are also a couple of scenarios relating to how to reverse payments received through Venmo.

Verify the Sender

Before any action, verify the sender’s profile. Ensure it’s someone you recognize.

Mistaken Payments

If you’ve been paid by someone you know by mistake or an incorrect amount, sending the money back typically resolves the situation. Once a payment enters your account, it’s final.

- If the entire amount is still in your account, it’ll be used for refunding, provided you can access the funds.

- If not, you can choose another payment method for the refund.

What to Do if You Sent a Payment to the Wrong Person

If you simply sent the wrong amount, then you can just request for the extra to be paid back. After all, you’ll most likely know each other and realize the mistake.

However, the situation can be a bit more difficult if you send it to the wrong person entirely. Chances are, you won’t know that person, and they won’t know you. They don’t have the incentive to give your money back.

Nevertheless, the first thing you should do when you send the payment to the wrong person is to ask for your money back respectfully.

Explain the situation, recognize your mistake, and apologize for the inconvenience you’re causing them. If they send the money back – then great! You don’t need to do anything else.

Requesting For Your Money Back

You can request to return your money with Venmo’s standard method. Here’s how you can do that.

- Open Venmo on your mobile phone.

- From your home screen, pick the “Pay or Request” button at the very bottom of the interface.

- Enter the username that you accidentally sent the money to (in the input field).

- It’s also recommended that you provide a short note on why you’re requesting that money.

- Type in the amount of money you sent by mistake.

- To push the transaction, tap Request.

- Tap the next prompt to confirm your transaction.

You can also send them a reminder if you think they’ve seen your request and note but forgot.

- On your Venmo app, tap the sandwich icon on the upper right corner of the interface.

- From the drop-down menu, tap “Incomplete.”

- You should then see different sections of transactions. Under “Requests,” you’ll see all the incomplete fund requests. Tap the Remind button below the request line to send them a reminder.

- The button will change to “Reminded” once your reminder has gone through.

How to Dispute a Venmo Payment

When you pinpoint a transaction that requires attention, it’s straightforward to raise a concern in the Venmo app. When doing so, pick the option that most closely mirrors your issue and provide as much detail as possible.

Follow this process:

- Navigate to the “Profile” tab.

- Identify and select the transaction in question.

- Tap on “Need Assistance?”

- Choose the description that fits your issue best.

- If there are other transactions you’re concerned about, tap on “Include more”.

- Once you’ve chosen all relevant transactions, tap “Proceed”.

- Tap “Continue”.

- Furnish any supplementary details.

- Click “Submit Concern”.

- If asked, update your app password for security reasons.

For concerns related to transactions made with the app’s Debit Card or online purchases, please directly contact the support team.

Important: Incomplete or vague details might prolong the resolution time for your concern.

What to Do if You Made a Duplicated Payment

If you made a duplicated payment, you could do the same process as the one above to help recover your money.

However, since a duplicated payment usually means that you sent the wrong amount to the right person, perhaps your chances of getting your money back will increase.

How to Contact Venmo if a Payment is Not Returned

However, if the other party is not responding or refuses to give your money back, you can contact Venmo Support. Venmo doesn’t guarantee that they’ll get your money back, but they will do what they can to help.

To contact Venmo support, follow the steps below.

- Go to their support hub and select the situation most applicable to your situation.

- You will then be directed to a page where you will submit a ticket by filling out the respective fields. Enter all the required information, such as your full name, phone number, registered email, and more.

- Write the nature of your concern under the “Tell us what’s up” field.

- Include attachments if you want. These can be screenshots of the payment you made, of your account, and the other party’s account.

- Click Submit.

Now you’ve notified Venmo support of your situation. Once again, this doesn’t guarantee that your money will be returned, but at least they will hear your complaint and do what they can.

You can also send them an email or chat with a representative with the Email us or Chat With Us options.

What to Do If You May a Payment to the Wrong Person

If you mistakenly made a payment to the wrong individual, you can reach out to Venmo’s support team, and they will assist you.

To facilitate a swift resolution, you’ll need to provide the support team with with the following details:

- Username of the recipient of the erroneous payment.

- Payment amount.

- Payment date.

- Intended recipient’s username, phone number, and email.

If your payment status appears as “Pending” due to sending it to an unregistered phone number or email, further guidance is available on addressing this issue.

Please be aware: Initiating a dispute for such payments won’t resolve the issue.

Best Lenders for Personal Loans

Avant (Best for Quick Approval)

Check rate

on partner page

on partner page

Avant Personal Personal Loan

Min. credit score

550

Fixed APR

9.95-35.99%

Variable APR

N/A

AmOne (Best of Low Credit Score)

Check rate

on website

on website

Upstart (Best for Fair Credit Score)

Check rate

on website

on website

OneMain Financial (Best for Good Rates)

Check rate

on website

on website

OneMain Financial Personal Loan

Min. credit score

None

Fixed APR

18.00-35.99%

Variable APR

N/A

SoFi (Best for Good Credit Score)

Check rate

on partner page

on partner page

Read More

- How to Add Money to Venmo

- How to Set Up a Venmo Account

- How Does Venmo Make Money?

- How to Close a Venmo Account

- How to Use Venmo

How to Cancel a Venmo Payment: Final Thoughts

The Venmo payment app can be an incredibly useful tool, so much so that almost all of us use it in our everyday transactions.

However, if you make a mistake in using this app, be prepared to lose your money. You can’t cancel or reverse a payment – although you can nullify your error by negotiating with the recipient. You can also contact support to notify them, but they don’t make guarantees.We have to deal with these situations if we want to keep on using Venmo’s admittedly excellent service. But if you want to close your Venmo account for good – that’s understandable too.

Sources ▼

- https://venmo.com/

- https://help.venmo.com/hc/en-us/

How to Cancel a Venmo Payment FAQ

Below, you will find some common questions about canceling Venmo payments, as well as other key topics, and their answers.

Can Venmo payments be reversed?

Once a Venmo payment is made to an existing account, it typically cannot be reversed. However, under certain circumstances, such as when the recipient gives explicit permission and their account is in good standing with the necessary funds available, Venmo Support might be able to assist.

How do I get a Venmo refund?

If you sent money to someone you know and need it returned, you should request the recipient to send you a payment for the same amount. They can use the “Pay” feature to return the funds. If it’s a merchant transaction, you’ll need to contact the merchant directly for a refund.

Can you dispute a Venmo payment?

Yes, you can dispute specific payments within the Venmo app. However, merely opening a dispute does not guarantee a resolution in your favor. Always provide as much detail as possible to support your case.

How can Venmo reverse a payment?

Venmo Support can only reverse a payment if:

- The recipient provides explicit permission.

- The recipient’s account is in good standing.

- The funds in question are still available in the recipient’s Venmo account.

How can I cancel a Venmo payment

Payments sent to an existing Venmo account cannot be canceled as they are available to the recipient immediately. However, payments sent to an unregistered email or phone number will appear in the “Pending” section, and you can cancel them from there.

Can you reject a Venmo payment?

Venmo doesn’t allow users to “reject” a payment once it’s received. If you get an unwanted payment or one by mistake, the best course of action is to send the money back to the sender.

How do I send money back on Venmo?

To return a payment:

- Open the Venmo app.

- Navigate to the payment in question under your transaction history.

- Tap on the payment to open its details.

- Use the “Pay” option to send the money back to the original sender.

What should I do if I sent money to the wrong person on Venmo?

If you mistakenly sent money to an unfamiliar person, immediately reach out to the recipient through the Venmo app requesting a return. If there’s no response or you suspect a scam, contact Venmo Support as soon as possible.

Rohit Mittal

Rohit Mittal is the co-founder and CEO of Stilt. Rohit has extensive experience in credit risk analytics and data science. He spent years building credit risk and fraud models for top U.S. banks. In his current role, he defines the overall business strategy, leads debt and capital fundraising efforts, leads product development, and leads other customer-related aspects for the company. Stilt is backed by Y Combinator and has raised a total of $275M in debt and equity funding to date.